Semaglutides: The Obesity Miracle Drug

While no panacea for weight loss, rising usage of Semaglutides among obese adults will have far-reaching effects on the US economy.

A recent analysis by Jeffries, an investment bank, estimated that if every passenger lost 10 lbs., then an airline could stand to gain $80 million a year in saved fuel costs due to the reduced weight of the aircraft.

Such market analyses come on the back of the introduction of weight loss drugs Ozempic and Wegovy (Semaglutides), which recently hit the market following successful clinical trials. The patients treated with these drugs over a two-year clinical trial witnessed an average body weight change of -15.2% compared to -2.6% for the control group.

At first glance the potential impact of the drug appears to be massive as the market size for obesity in America is huge – about 30% of American adults are obese— and the number is growing every year (see section on market size).

But like Nicorette, there is only so much a *miracle* weight loss drug can do. For one, patients will need to take the drug indefinitely to maintain weight loss. Second, over time the patients who take the drug will likely develop a tolerance to it, rendering it less effective. Third, the drug comes with side effects, which may dampen its use. And lastly, in the immediate term the high cost of the drug (>$10,000 a year) will likely deter many users from taking the drug and insurers from covering it. (See section on barriers to adoption for more detail).

Nevertheless, assuming the above barriers prove to be minor or temporary, the long-term effects on the market will be significant, from reduced costs for airlines (fuel costs) to reduced demand for specific types of food and drink products, to downstream effects in the food, beverage, and grocery supply chains (in the last section I dive a bit deeper on the fast-food industry). Indeed, firms like Walmart have stated that they are already seeing the effects of the drugs on consumer demand.

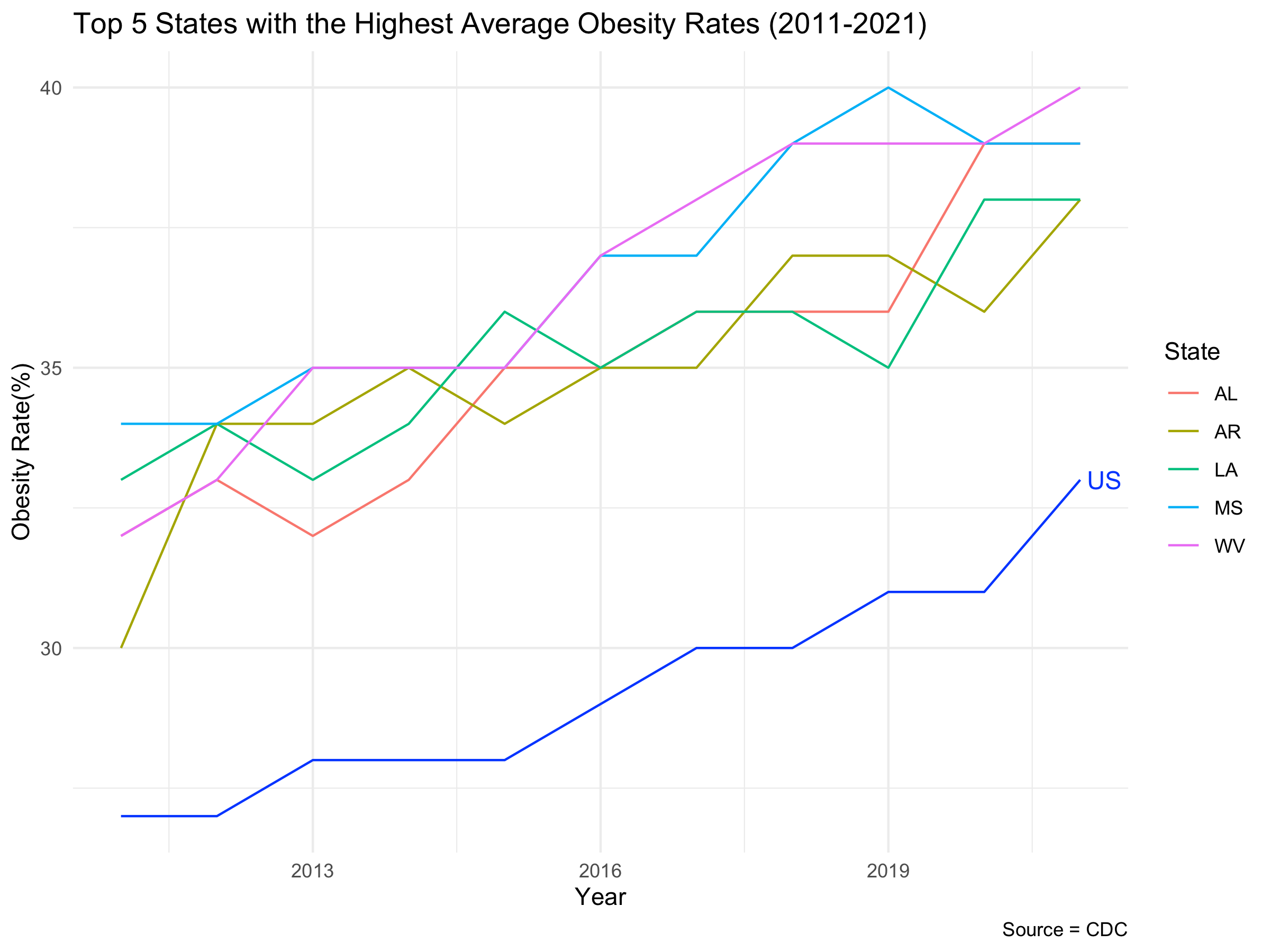

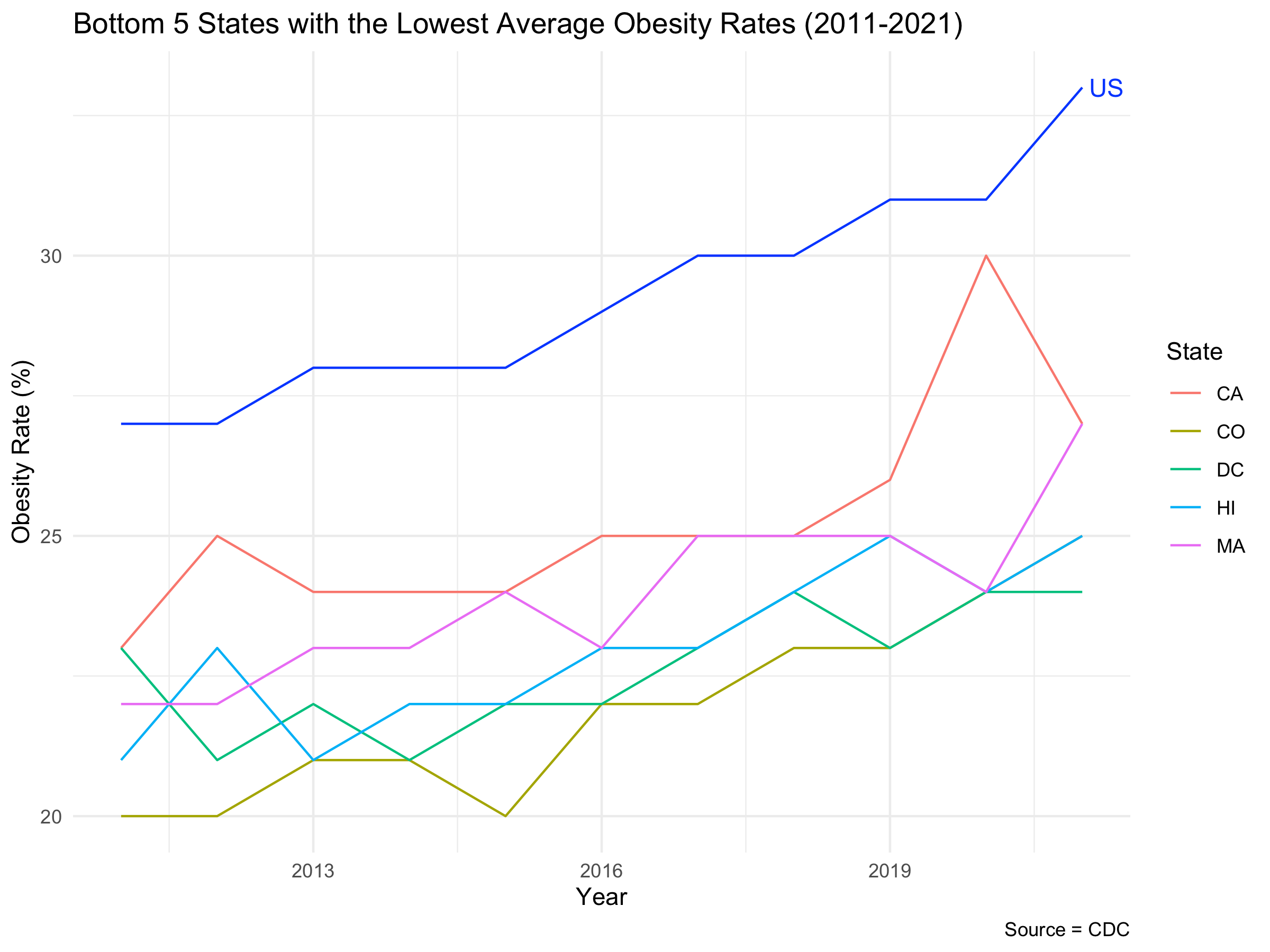

Market Size: Obesity in America

Figures 1-3 give a broad view of the market size of obesity in America. For example, one can see that obesity rates have been increasing across the country, which can partly be explained by a population that is aging—in 2011 the median age was 37.2, while it was 39.7 in 2019 (Figure 1).

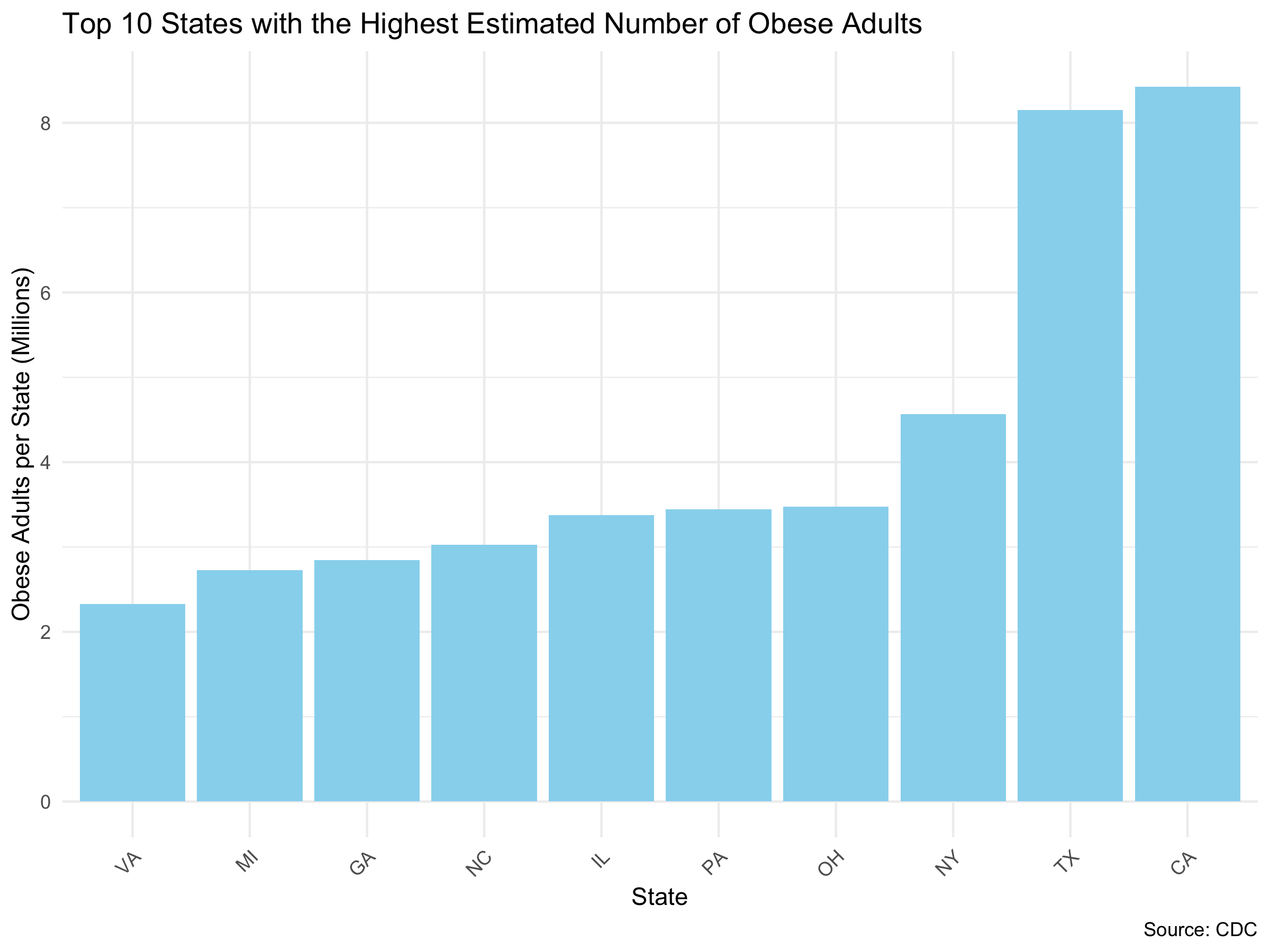

Specifically, in some of the most obese states such as Alabama and Arkansas, obesity rates were closing in on 40% of the adult population in 2021, while for the least obese states, they have been creeping up to 25% of the adult population (Figure 2). It’s also worth noting that while some states like California have some of the lowest obesity rates, their large population sizes mean that they also have some of the largest counts of obese adults in the United States (Figure 3).

Short to Medium Term Consumer Adoption

Ok so the market size is massive and will likely continue to grow. But what slice of this market will adopt the drug?

Supply

Currently drugs such as Ozempic and Wegovy are approved to be prescribed as treatment for type 2 diabetes, which afflicts about 8-11% of the total population. Doctors can also prescribe the drug for weight loss on a case-by-case basis, but most insurers are not covering for weight-loss, meaning that most patients would need to fork out about $10,000 or more a year on prescriptions.

However, even with these drawbacks, demand for the drug is still far exceeding supply.

Demand

Cost Barriers

Naturally, in the medium-term supply will catchup as manufacturing is ramped up, but how will demand change? I think it’s fair to assume that at some point the cost to the average patient will drop significantly (rise of generics, reduced manufacturing costs, etc.), which will lead to far greater adoption of the drug. Indeed, a survey conducted by KFF health found that 45% of adults would be interested in taking a safe and effective weight loss drug, but that this interest drops to 16% if the drug was not covered by insurance.

Non-Cost Barriers

Administration

Currently, one of the main barriers to adoption is the need for patients to administer the drug intravenously. In the same survey from KFF health, only 23% (of 45% originally) of adults were still interested in taking the drug once they found out they had to administer the drug intravenously.

Dosing for life

The secondary barrier is the need to take the drug indefinitely to maintain weight loss. According to the results of a randomized control trial published last year, patients who stopped using Ozempic after 68 weeks of treatment gained two-thirds of their prior weight loss. Indeed, in the same KFF survey when patients were told that they would have to take the drug indefinitely, interest in adopting the drug fell to 14%.

Side effects and drug efficacy over time

Finally, it is still unclear what percent of patients will experience side effects (and as a result stop their prescriptions). In clinical trials 44% of patients experienced nausea and 31 percent had diarrhea among other side-effects. What is more, it remains to be seen how effective the drug is in enabling patients to maintain weight loss over an extended period of time.

In short there are several factors that could affect how deeply the drug penetrates the market in the short to medium term: the price of the drug, barriers to adoption, costs to continue using the drug (increasing dosage due to increasing tolerance), side effects, and most importantly the percent of patients that stick to the treatment indefinitely.

Industry Impacts of Increased Adoption: An Example

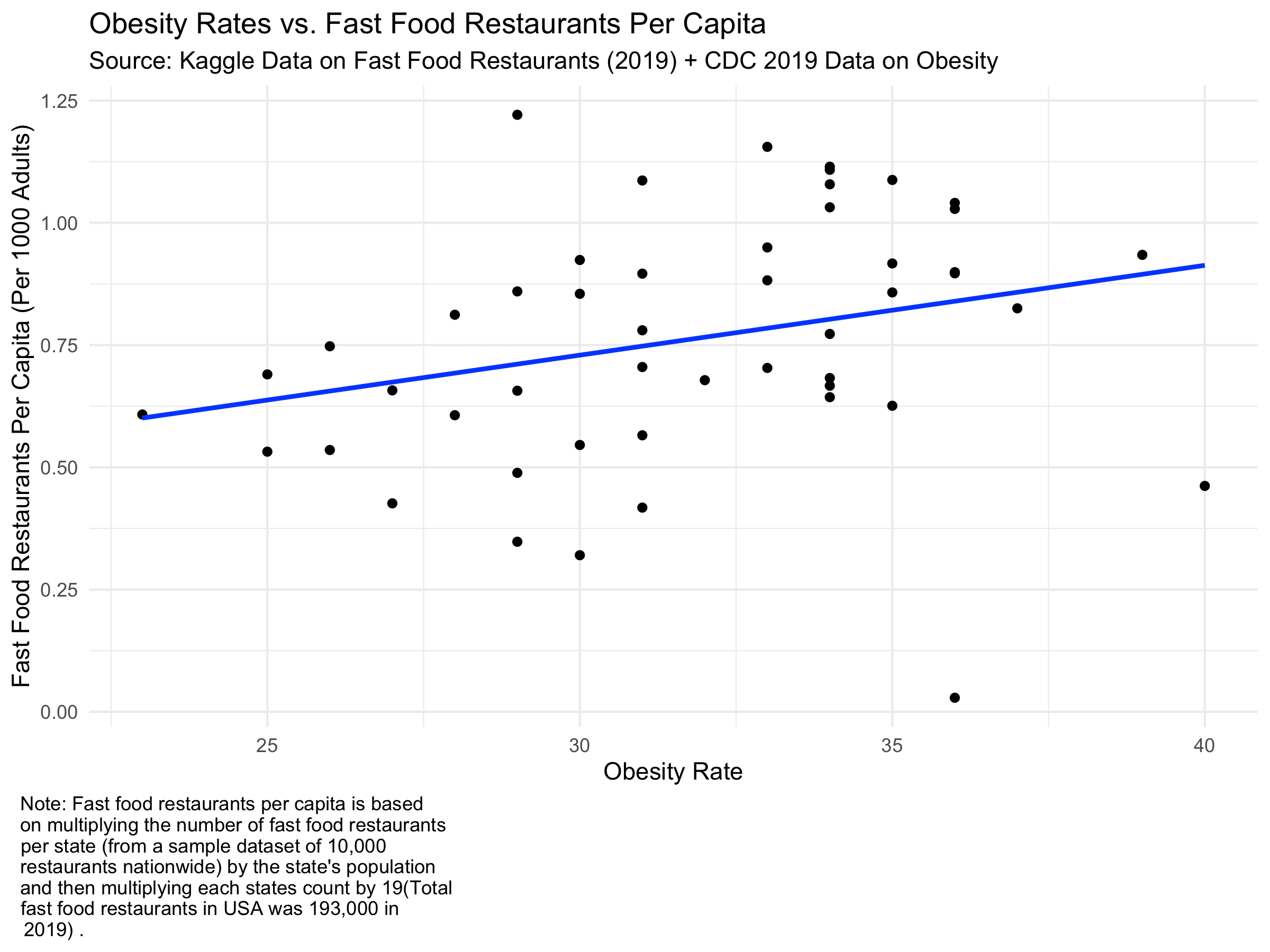

How will increasing adoption of Semaglutides affect local industries? One clear example is the quick-service industry in the United States, which Statista estimated to have reached a total market size of $330 Billion in 2022. Will states, in which a significant percent of obese adults adopts these drugs, witness exits of fast-food chains in their local markets? It is very plausible.

For example, in the Figure 4, I show fast food restaurants per capita against obesity rates in 2019, where one can see a moderate and positive relationship between fast food restaurants per capita and obesity rates across America.

Exits of fast-food restaurant locations across the United States will naturally lead to knock-on negative effects downstream in the supply chain from producers (e.g., Keystone), hospitality cleaning product providers (e.g., Ecolab) and food and beverage distributors (e.g., Sysco), and spirits, wine and beer makers (e.g., ABinBev, Pernod Ricard) and distributors (e.g., Southern Glazer). What’s more, in states where adoption rates of Semaglutides are highest, one would also expect reduced demand for fast-food workers. According the Bureau of Labor Statistics, the QSR sector employs ~4.5 Million food service workers nationwide.