The Student Debt Repayment Shock

In June 2023 the Supreme Court voted against the Biden administration’s proposal to forgive up to $20,000 in student debt per individual debtholder, which if implemented, would have forgiven an estimated $440 Billion of Federal Student loans, impacting a total of 38 million borrowers across the country.

Since then, debtors have been paying down their student loans in droves, as demonstrated in the Figure 1 below. Preceding this, one can also see two other events of interest: 1) A drop in loan repayments after March 2020—at the start of the pandemic the Biden Administration paused interest and accumulation on student loans as an emergency relief measure; 2) A further drop in loan repayments following the Biden Loan forgiveness proposal in August 2022.

Specifically, students lowered their debt repayments from March 2020, and then lowered them even more with the expectation of debt forgiveness. As such, the restart of loan repayments will come as a significant shock for this cohort of Americans, and will no doubt have major implications on their spending, borrowing, and saving in the months to come.

What’s more, the student debt repayment shock also comes at a time of rocketing credit card debt and a loosening white-collar labor market both of which exacerbate the problem.

For credit card debt, as shown in Figure 2, balances are at almost a $1 trillion, up from around $850 Million pre-pandemic.

And with regards to the labor market, we can also see that things are not so rosy for student debt holders. This is best demonstrated in LinkedIn’s hiring trends, which one could argue are the best proxy for labor demand for white-collar workers—postings on Linkedin are typically for jobs that require a college degree or higher. Specifically, Figure 3 shows that overall hiring on Linkedin was below pre-pandemic levels in August 2023 and trending downwards.

Deep Dive: Who Has Student Debt?

In short, from the story above, the picture doesn’t look great for student debt holders. But what does it look like at a detailed level?

To elucidate this question, I reviewed data from the Federal Reserve Board of Governors’ Survey of Households to get a more detailed view of the average student debt holder and, to better understand the financial situation of student debt holders.

The survey includes a range of questions (demographics, income, debt, financial well-being, etc.) with a primary focus on household finances. The survey was conducted in October 2022, not long after the Biden Administration’s debt forgiveness proposal, and includes responses from 11,000 adults.

High Level Data (Individuals with Student Loans)

To start, here are few high-level stats on student debt holders. First, 15% of respondents in the survey hold student debt. Of those individuals:

57 % White and 20% Black vs. 69% White and 11% Black for all respondents

47% under the age of 35

36% Bachelor’s, 29% Master’s, 34% some college (i.e., have Associates degree or partially completed bachelor’s degree)

Mean Income: $80,000, Median = $65,000

In short, student loan holders are on average young, disproportionality black and a mixture of undergraduate, advanced, and non-degree holders. They also have household incomes that hover around the mean/median household income in the United States.

Debt and Income Among Student Loan Borrowers

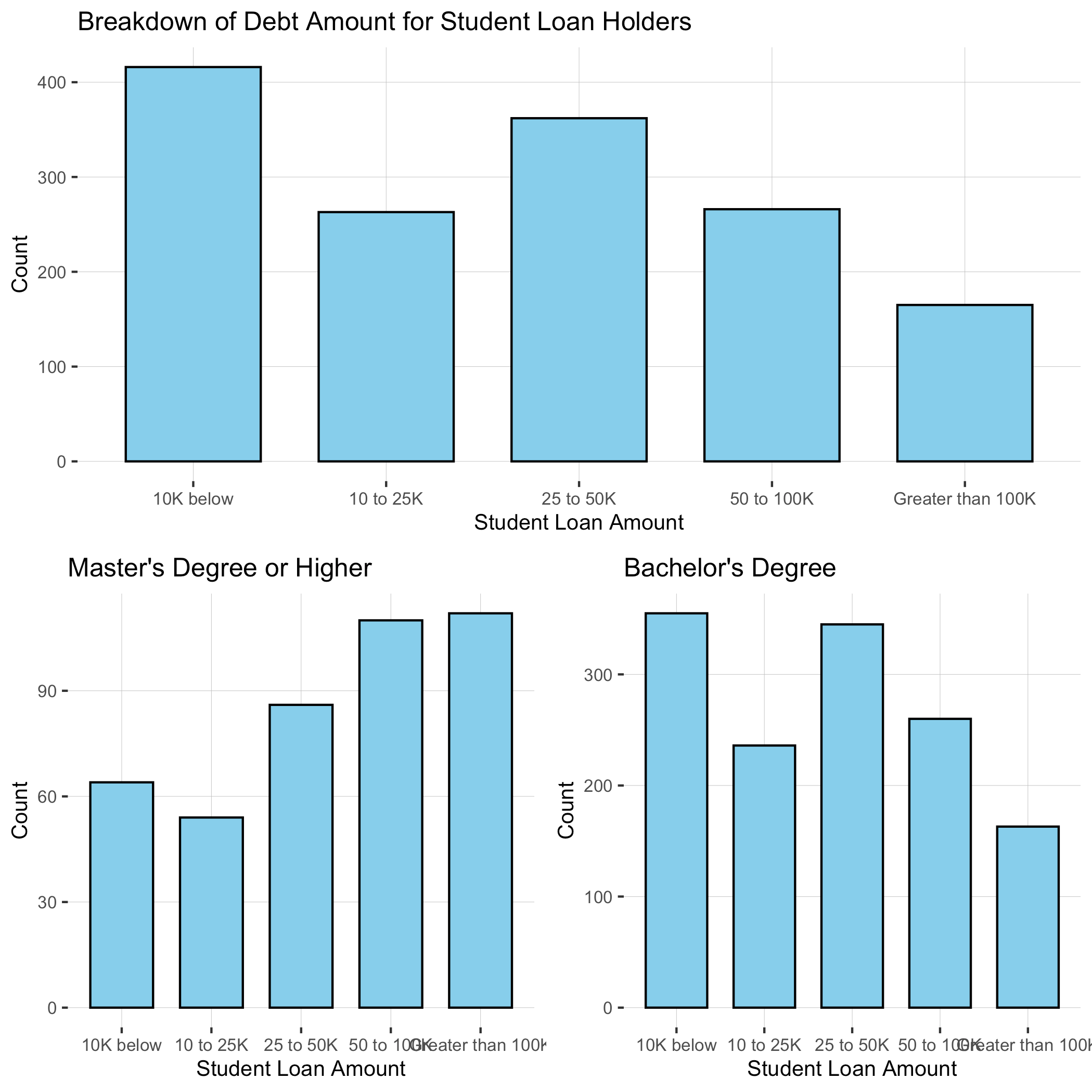

Next comes the meat—how are these individuals doing financially. To start, I analyzed the breakdown of student debt amounts among student loan holders. In line with prior research, I find that individuals with a master’s degree have higher debt burdens than individuals with a bachelor’s degree or just some college education (Figure 4).

Then I looked (at a high-level) at whether individuals with student debt were facing other credit constraints. Here is the breakdown:

Spending

7% borrowed from money retirement savings (past 12 months)

15% have struggled to pay bills (past 12 months)

25% spending more than their income (past month)

Credit

49% have credit card debt they don’t expect to pay next month (compared to 30% for respondents with at least some college)

24% have increased their level of credit card debt since a year ago (compared to 13% for respondents with at least some college)

Of the above, the main data point that sticks out is credit card debt. Specifically, almost half of the respondents who hold student debt are not regularly paying off their credit card debt. What strikes me about this is that the survey was conducted a year after the pause on loan repayments and interest, and right after the Bidens proposal to forgive student debt. This begs the question as to how much more credit card debt these individuals will amass in the months following the restart of student loan repayments.

Moving on to the income side, first I confirm (again in line with prior research on the college wage premium) that there is a positive relationship between the level of education obtained and household income (Figure 5).

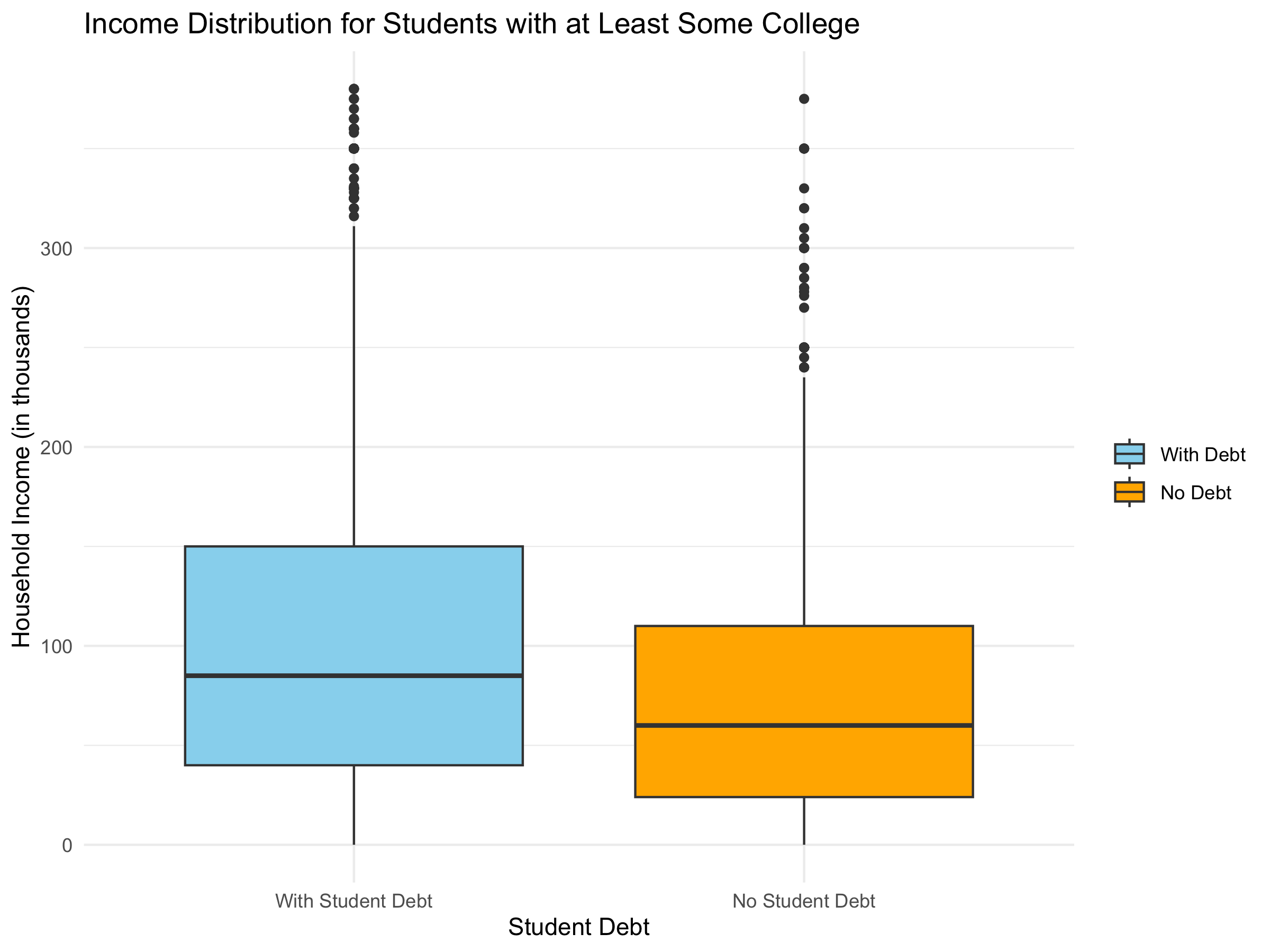

Second, I find that the average student debt holder has a slightly higher income distribution than that of the non-debt holder. This makes intuitive sense given the fact that students with debt are more incentivized to take on jobs/careers with high salaries so that they can pay down their debt more quickly. These findings also do not change markedly when only sampling individuals with a bachelor’s degree or higher, as shown in Figure 6.

Finally, I evaluate whether individuals with more student debt also had higher incomes, finding that the distributions are largely similar across different levels of debt (Figure 7). Specifically, one can see that there is positive correlation between the level of student debt and household income, but the relationship is weak at best. And, when only looking at respondents with a bachelor’s degree or higher, there appears to be no relationship at all (Figure 8).

Conclusions

At a macro level, reduced demand for college-educated workers (fewer Linkedin job postings), coupled with the restart of loan repayments will create significant headwinds for student debt holders.

The review of household survey data from late 2022 also supports the macro view. Specifically, I find that among respondents with at least some college education, student debt holders had on average higher incomes than non-loan-holders but also struggled more to pay down their credit card debt. Based on this, one would expect credit card debt among student debt holders to increase following the resumption in student loan repayments.

In addition, looking within the cohort of student debt holders, I find a linear and positive relationship between the level of education obtained and household income (this is in line with the broader research on the college-wage premium).

On the other hand, I find little or no relationship between household income and the amount of student on an individual’s balance sheet. This likely means that there is a large percentage of student debt holders that have debt burdens that are not manageable with their existing incomes.